To access the full survey results click here.

In its Winter 2017 edition, Global Custodian published a feature titled “Battleground 2020: ETFs”. The overarching theme of the article centred on the surge in uptake of passive investing, resulting in exchange traded funds becoming one of the dominant asset classes for the buy-side, a shift in possibly determining the next top global custodian.

Since that article was published, assets under management (AUM) for ETFs have increased from $4.4 trillion in September 2017 to $6.1 trillion as of the end of May 2020. The low-cost nature of ETFs – in comparison with mutual funds – have made them an attractive feature for all investor types, sparking their ascent to become one of the most popular investment vehicles.

As noted in a previous edition of Global Custodian, the dramatic changes at the client level will most likely send ripples to everyone involved in the investment servicing process, due to the heightened level of transparency and efficiency associated with the ETF market.

Having looked at where the market was heading – not to mention the increased frequency in ETF-related asset serving headlines featured on Globalcustodian.com – plans were hatched to launch a new survey assessing the level of service provision of custodians and fund administrators in this market.

With this being Global Custodian’s first brand new survey for several years, the questionnaire was developed following extensive consultation with ETF industry experts to deliver a set of questions that not only focused on the standard functions of a custodian and fund administrator – such as client service, fund accounting, middle-office, technology etc – but also on more specific services related to ETFs – such as basket services, reporting to institutional investors and authorised participants, and ETF servicing models.

After a soft launch in April, the survey gathered responses from 79 ETF issuers and authorised participants globally, representing over $2.3 trillion in AUM. Five responses were the minimum sample number required to assess a service provider adequately enough to publish their average scores, both in absolute terms and relative to the average scores in each service area.

ETF service providers play a key role in facilitating the primary market process through their roles as transfer agent, fund administrator and custodian. They also help Authorised Participants – otherwise known as market makers – fulfil their role in providing liquidity and reducing the overall costs for investors.

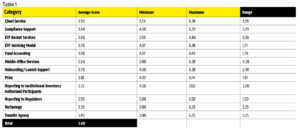

Table 1 indicates the average collective scores by service category of the eight providers that were rated individually in the survey, as well as the differential range of scores provided in each category. Overall, respondents as whole fell felt that their business is well served by their ETF administrators and custodians with all categories rated in the ‘Good’ range.

Regulatory reporting achieved the highest average score (5.95) but also with the lowest range (1.50), suggesting this function is handled similarly between providers. The recent wave of regulation across the ETF space – most notably Rule 6c-11 (also known as the ETF Rule) in the US, MiFID II in Europe, and the approval of active ETFs in Hong Kong – has made reporting standards an imperative for providers.

Similarly, ETF servicing models and Reporting to Institutional Investors/Authorised Participant received high scores but with a narrow range, suggesting many of these services are performed at a similar standard across providers.

The largest range was seen in ETF Basket Services and Middle-Office Services, where providers can tap into value-added services for these functions to differentiate their offering. Meanwhile, Price received the lowest average score, but with a narrow range. This suggests there is a generally accepted price level across providers.

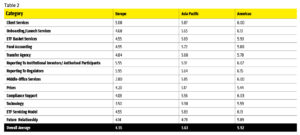

Table 2 shows the average scores by region, of which providers received higher ratings across the board in the Americas. This is hardly a surprise given the fact that ETF servicing has been able to mature over a longer time period in comparison to the Asia-Pacific andEuropean markets. Middle-Office services by providers in Europe, however, were rated particularly ‘Poor’, and Technology and Compliance Support also received low scores. However, the European ETF market is continuing to evolve and the migration to an international central securities depository (ICSD) settlement model will help providers and ETF issuers overcome challenges of fragmentation.

Going forward, providers will be challenged to scale and mature services for this ever-growing market. The migration of active to passive investment is driving a greater need for efficiency, and providers will have to continue demonstrating how they can deliver an end-to-end service offering to asset managers, while also reducing the total cost of ownership for the investor.

We at Global Custodian hope this survey will provide an indication of how the ETF industry benchmark their service providers, and we look forward to expanding this survey to more providers in the years to come.

To access the full survey results, follow this link.